The second Forensic Audit Report prepared by the accounting firm of Grant Thornton has now been released to the public. It will constitute the major focus of Phase II, the “Construction Phase”, of the Commission of Inquiry into the Muskrat Falls Project (MFP).

This Report builds on the main conclusions of the first one released in September 2018, prior to the beginning of public hearings presided over by Judge Richard LeBlanc. It concluded that, at the time of sanction, a “combination of…potential misstatements may have resulted in the Interconnected Island Option (the Muskrat Falls project) no longer being considered the least cost option at the time of sanctioning.” In other words, had the Cumulative Present Worth (CPW) – the present value methodology used to compare the Isolated Island and the Interconnected Island options – been objectively assessed, the Muskrat Falls Project was probably not then, or ever, “least-cost”.

What had GT uncovered in order to come to that conclusion?

Those findings and observations were repeatedly confirmed in testimony given by multiple Witnesses at the Inquiry, including from Nalcor’s key Consultants.

|

| Inquiry Commissioner, Judge Richard LeBlanc |

The “Base Estimate”, prepared by SNC-Lavalin personnel, under the direction of Nalcor’s Deputy Project Director, is said to have constituted 70% of the total project Estimate. The other 30% was calculated solely by Nalcor. Together, the figures comprise the DG3 numbers used to sanction the project.

At the outset, we would suggest that the revelations of the Forensic Auditor constitute a serious indictment of the honesty and integrity of Nalcor, as a publicly-owned Crown Corporation. The evidence confirms that until Stan Marshall became CEO of Nalcor and offered up a forecast final cost that was based upon the project’s escalating cost history, the public was largely kept in the dark.

It is worth reminding readers that former Premier Dunderdale acknowledged during her testimony in December that she was made aware by former CEO Ed Martin, prior to sanction, that a $500 million overrun was possible. The GT Report confirms that that figure – the threat of which ought to have been a showstopper - was overtaken within just four months after Sanction. The excerpt (below) from GT Report (p. 13) provides this confirmation.

(CH0007 refers to the Astaldi contract for the intake, powerhouse, spillway and transition dams. CT0327-001, referenced later, is the Vallard combined work package for the Transmission Line (known as the Labrador Island Link, LIL, which does not include the line between Muskrat Falls and Churchill Falls, known as Labrador Transmission Assets, LTA, and for which the contract was also awarded to Valard!)

“Nalcor was aware that their original schedule was aggressive”, says GT, based upon a DG3 Cost and Schedule Risk Analysis Report, dated October 2012. The Dunderdale Government gave Nalcor Project sanction in December 2012. With almost no hope of being met under any circumstances, the Construction Schedule was compressed because “Financial Close” had not been achieved.

The “Financial Close” provision required that the Province meet all the conditions of the “Term Sheet” for the Federal Loan Guarantee (FLG) before Nalcor could access the billions of dollars required to finance the major contracts and proceed with the project. In particular the Utilities and Review Board of Nova Scotia had to give its approval for it to become a “regional” project deserving support from the national government!

At the time of Sanction, the Feds and the Province were still negotiating the Federal Loan Guarantee. In addition, Release of the Labrador Island Link Transmission Line (LIL) Environmental Assessment, expected in April 2013 (which, strange as it may sound, was separate from the work of the Lower Churchill Environmental Panel), did not actually occur until November 26 – a delay of six months. Effectively, GT reports, the date for first power was shifted from June to December, 2017 and the date for full power six months later.

The mention of the date of delay in “Financial Close” is important for two other reasons. Firstly, it delayed the award of the Astaldi contract to just ahead of Winter 2012/13 which was disastrous for a company that, arguably, should not have been awarded the contract in the first place.

GT quotes Don Delarosbil, Astaldi Project Manager, offering this explanation: “if you start in November instead of June you’re not just losing four months, you’re probably losing ten months. You almost lost a year of construction”. (P.12)

The second reason that the date of “Financial Close” is important is that the delay afforded Nalcor, then in possession of several large bids for work packages, created absolute certainty that its “Base Estimate” was far too low!

In effect, Nalcor was given a timely opportunity to cancel the project. GT states: “Nalcor had the ability to stop construction without funding the remaining cost to complete. However, once the FLG was executed Nalcor/GNL were committed to funding the project” including the cost overruns. The likelihood of such a cancellation, however, diminishes with evidence contained in the Forensic Audit that Nalcor had committed approximately $900 million to the project prior to the date of Financial Close. (p.10) Nalcor had adopted the flawed concept of sunk cost which meant that they believed the project must not be stopped once such a major commitment had been made. This led them to ignore all the red lights which should have compelled them to seek an “off ramp” to terminate the project!

The Inquiry is not just about the decisions of Nalcor; it is about those taken by the Government. A key question is whether the Crown Corporation had fully informed the Dunderdale Government, prior to Financial Close, that bid prices had exceeded budgeted amounts and that an underfunded contingency allocation had already run out and that overruns of 25% had already been recorded? Following on that question is another: if the Government was informed, did they initiate appropriate reviews to better define the risk to the province and assess if the project should be shut down, in consequence of that risk?

Not surprisingly, the GT Report offers mounting evidence that the Government of Canada knew or ought to have known that the Muskrat Falls project was a financial travesty that would economically endanger the province. Rightfully, the IE will be examined during this phase of the Inquiry at which time he will be asked to address what he knew and the role he played in informing the Government of Canada. As a start, we will need to know if and when he informed the Federal Government not just of Nalcor’s financially flawed project but also regarding the impossible schedule – one that had seriously slipped by the time of financial close.

Phase I of the Inquiry had confirmed that Nalcor knew, having been made aware both by its Consultants and the IE, of a plethora of project risks. The IE warned Nalcor, for example, “that the contingency they selected for the LCP (less than 7%) was less than the low end of the range of what the IE typically sees at comparable DG3 stage gates.” (P.16)

Apart from Nalcor, if the Federal Government was also informed, did they just turn a blind eye to the potential consequences for the Province, the latter having signed a completion guarantee? It was the completion guarantee that placed the financial obligation to complete the project on the back of the province!

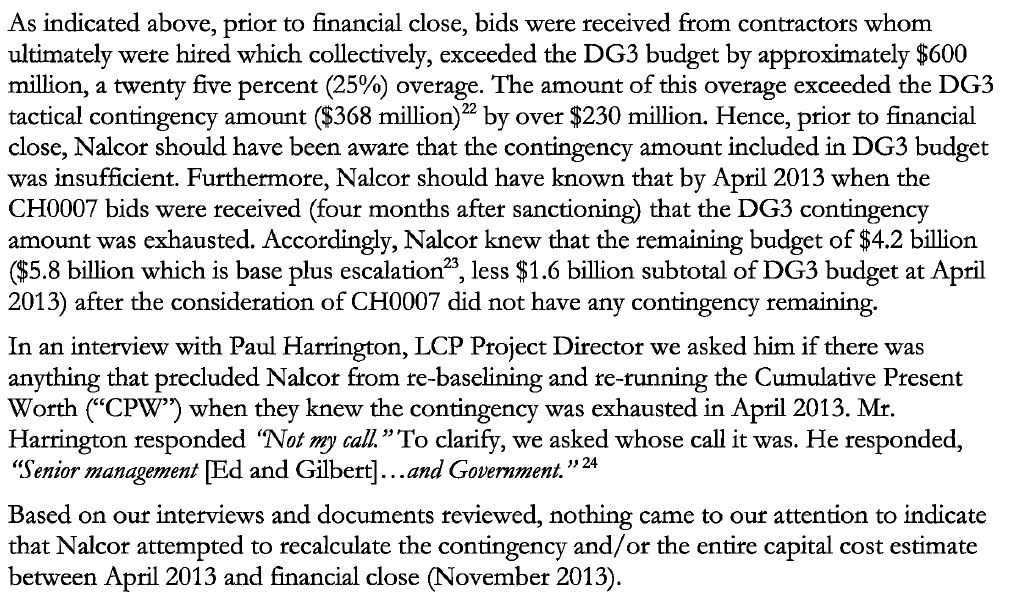

That issue notwithstanding, there is still Nalcor’s “dam the torpedoes” approach to obtaining Project Sanction. The Forensic Auditor states that “Nothing came to our attention to indicate that Nalcor attempted to recalculate the contingency and/or the entire capital cost estimate between April 2013 and financial close (November 2013).” Underlining the point, GT notes that “At the time of financial close, the project schedule was delayed by six months, demonstrating that the 97% chance of schedule slippage determined at sanctioning was in fact materializing.” (P.17)

One other thing is clear: while Nalcor's Project Management Team (PMT) monitored the forecast growth in cost to complete the project, on at least one occasion – March 2014 – GT observed that Nalcor did not include in the estimate “forecasted costs due to Alstaldi's performance and delays”. GT stated that this failure was contrary to best practices. GT also noted “there were instances where the Nalcor Executives knew that the cost for the project increased months before the budget increase was approved by the board of directors…”

While V-P Gilbert Bennett and CEO Ed Martin were kept informed, we also know that they never shared up-to-date information with the public.

During this Audit, GT reviewed six work packages (see Exhibit below) having “variances which exceeded $100 million”. The review covered the reporting period which ran from the original sanction budget ($6.2 billion) to March 2018 when the forecast final cost was $10.1 billion plus financing costs. The reader will note that the final details of three of the six work packages have been redacted for reasons of “commercial sensitivity”, the contracts still on-going. Our summary and comment will, therefore, be limited to the three contracts fully considered by GT. Taken together, the three - CH0007-Astaldi, CT0327, and Engineering, Procurement, Contracting and Management (EPCM) -represent 61% of the total cost overruns of $3.915 billion. All six contracts are listed in the Exhibit below.

Astaldi

The Astaldi Contract (CH007) was the largest tendered Work Package on the project. GT notes that as of March 2018, at which time the project was suffering overruns of $3.9 billion, Astaldi accounted for 31% of the overruns or $1.2 billion.

The Astaldi Contract will come under severe scrutiny in the coming weeks not least due to its unsuitability to do the work. The question that has always needed clarity is this: who made the decision to award them the contract and why?

Nalcor disregarded two higher bids from Canadian companies – the only two having project knowledge of construction in Labrador’s sub-Arctic conditions.

Of the nine companies that answered the prequalification invitation, four of them were selected to participate in a Request For Proposals (“RFP”). The two Canadian companies were AeconJV, IKC and two foreign companies: Astaldi and Salini JV. The Bids were received on April 16, 2013. The Exhibit below shows the Bid prices received and, importantly, the number of labour hours contained in each Bid price.

Outside of the failure to include adequate contingency allowances, the project was challenged by an impossible project schedule, an unqualified Nalcor senior executive and an inexperienced project management team. The selection of Astaldi only magnified those deficiencies. The Commission of Inquiry will need to be focussed on them because key management issues often get lost in a barrage of rhetoric from self-serving Witnesses. This is the same stuff that just a few years ago helped acclaim those executives as “international experts”.

The Astaldi debacle is multi-faceted and is best understood only if certain key questions are addressed to the Company and to the Forensic Auditor. They include: what factors were assessed in the pre-qualification process other than the Bid price and what weights were assigned? What weight was given to construction experience in northern climates, to previous experience in building hydro-electric projects globally, and to working with indigenous people? What references were sought from other clients of Astaldi? What weight was assigned to depth of their financial resources?

GT’s analysis of the Bids, not surprisingly, deals almost completely with the number of labour hours included in each Bid (line 2 of the above Exhibit) in order to complete the work. This is the “productivity” issue around which hangs the issue of cost overruns and questions related to “low-balling” of the Estimates. Those assertions were made by the gentleman known as the “Anonymous Engineer” who had worked in this area of the project.

GT observed that “The total labour hours included in the four bids ranged from 5.85 million to 9.51 million, an increase ranging from 60% to 160% over the DG3 estimate.” (P.28) Nalcor’s DG3 estimate “included 3.66 million labour hours” in contrast to 6.83 million hours included in the Astaldi Bid – a difference of 3.17 million hours (see Exhibit below).

Over the years many have expressed exasperation that a company as inexperienced in sub-Arctic conditions as Astaldi could be selected to carry out a megaproject in the wilds of Labrador. When a more experienced Owner would have disqualified the contractor at the pre-qualification stage fearing the obvious, Nalcor’s scoring system for contractor selection favored the lowest bidder. Stated GT, “regardless of lower scores in execution of the work”….both Salini and Astaldi “were selected for further consideration.” (p. 28)

Unfortunately, the Report exhibits large gaps of analysis including, among others, an assessment of the contract language that wedded Nalcor to Astaldi and the opportunities it afforded for extra billing. We are left to assume that the mistake of selecting Astaldi could not be remedied, a swift firing having been perceived as too expensive. However the failure to act on a timely basis in removing Astaldi from the job was an egregious lapse on the part of the new CEO and his management team, which they acknowledged when in November of 2018 they reached the inevitable conclusion that Astaldi must be replaced!

It also appears that the contract contained both “lump sum” and “unit priced” components, the latter exposed to interpretation and inflation. Who cannot remember CEO Ed Martin’s varied characterization of the contract as a lump sum contract with incentives for performance, leaving one to wonder what Astaldi and the public purse had actually bargained for?

That said, GT confirms that “once Astaldi was chosen…and work commenced, costs grew significantly. The overrun, as of March 2018, was attributable to the bridge agreement and completion agreement, change orders and unallocated scope.” (p. 29) GT states: “The Astaldi contract was signed on November 29, 2013 (the date of financial close) for $1.024 billion (excluding an adjustment of $64 million). After taking nearly a year to ramp up for the work, by mid-2015 Astaldi was soon in deep financial trouble.

Nalcor was now faced with saving a poor performing Company.

Grant Thornton confirms that Astaldi had completed a “less than expected production rate of concrete placement and being behind schedule…” An internal analysis conducted by Nalcor in mid-2015 “concluded, that based on the amount of funds spent on labour during 2014 there was a significant cost gap and that it could range from $500 million to over $800 million to complete the scope of work.”(p.30)

What followed were a series of agreements with Astaldi in an effort to keep it solvent including a ‘supplemental’ agreement and a ‘bridging’ agreement. GT does not inform us if Cabinet approval was sought on those agreements or if Government’s agreement to underwrite any requests from Nalcor for contingent equity sufficed. The GT Report notes that cash advances were made to Astaldi but we are not told why or if the Government was informed and approved of them. These unusual cash advances had been pointed out by a “naysayer” at Nalcor’s AGM!

As noted already, the issue of productivity is prominent in the Report, in relation to Astaldi and hence, to the problem of cost escalation. Astaldi’s scope of work required that it pour approximately 478,000 cubic meters of concrete. Astaldi had assumed a conservative 6.57 direct labour hours for each meter of concrete poured, in contrast to Nalcor’s 4.50 labour hours (see Exhibit below). However, even the Astaldi estimate did not come close to the actual direct labour hours required per meter of concrete. According to the Forensic Audit the number never went below 14 “direct” labour hours per cubic meter of concrete. The Indirect labour hours have a wide variance with Nalcor’s DG3 estimates, too, making Nalcor’s claim to a sound “Base Estimate” arrant nonsense.

GT adds another statistical note which, alone, magnifies the futility of the goal the Company thought it might achieve. Says GT, in order to meet the schedule, “Astaldi on average would have had to place approximately 13,300 m3 per month (478,000 m3/36 months) cubic meters of concrete each month, including the winter months. This production level was attained nine times out of 57 months since commencement of the project in November 2013 (through August 2018).”

A Study conducted in 2015 by the Ibbs Consulting Group, Inc. for Astaldi and Nalcor on the problem of productivity reported that “Labor productivity is degraded on Muskrat Falls by too much waiting time, too much rework, and not enough overall site coordination.”

It is noteworthy that while the Astaldi contract allowed for 1 million more "direct" labour hours than did the Nalcor estimate at sanction, Nalcor had allowed in its Base Estimate the cost of an Integrated Cover System ("ICS"), AKA the “Dome”. According to GT, the ICS was supposed to “allow the workers to work comfortably inside the structure during the winter season resulting in no loss of labour productivity due to the climate.”

The “Dome” was demolished even before it was completed. As to whether it made any sense from an engineering perspective, GT’s Consultant makes this observation (p. 39):

“Not common and warranted detailed scrutiny”. Did the idea of the “Dome” originate with Astaldi? Did Nalcor buy into the idea without first assessing its merits?

GT cites the Williams Engineering Report (page 38) stating that Astaldi was the only bidder who planned to work through the winter. The obvious question: was this poorly understood and expensive idea a major factor in the selection of Astaldi as the preferred bidder? While an uninformed public will certainly want to know who paid for the $100 million plus debacle, they also have a right to know, the “Dome” having failed, whether Nalcor pushed Astaldi to work through the winter at enormous expense and the knowledge that productivity was negligible.

Fearing “Astaldi’s (poor) financial strength, i.e. their ability to absorb losses of such magnitude” Nalcor soon found itself required to consider paying Astaldi “additional compensation in the amount of $743 million”. Exhibiting its own lack of management depth, Nalcor sought out the assistance of Westney Consulting to perform “an analysis to determine the best course of action.” Westney essentially concluded that paying Astaldi represented a better alternative than replacing Astaldi. And so (costly) negotiations soon got underway to help keep Astaldi afloat.

Nalcor entered into a “bridge agreement” initially with Astaldi as negotiations continued over the whole amount claimed. It is important to note that “effective as of December 1, 2016….The total contract price was $1.83 billion…inclusive of the scope of the original contract and all change orders up to and including November 30, 2016. “...another $78 million for additional travel and escalation related to the completion contract”, was also added. The “settlement”, states GT, “of $884 ($806 million+$78 million) resulted in a total package budget of $1.908 billion related to the completion contract.”

After that settlement, states GT, costs “continued to increase to $1.959 billion as of March 28, 2018…attributed to a variety of change orders…” following which, on October 22, 2018 Nalcor “issued a stop work order to Astaldi”.

For readers wondering where at least some of their money went, overruns paid to Astaldi are reiterated below:

So many questions await both Nalcor and Nalcor that it is possible to mention only a few others.

For example, there is no reference in the Report to incentives for higher productivity. Did the collective agreement limit their use? Did any of the bidders bring forward an incentive based system which rewarded productivity either on a shift or individual basis?

Were productivity data used by management to design an incentive based system which might have provided bonuses to direct labour and to supervisors, too? Were penalties imposed on Astaldi when they failed to meet production targets?

EY, in its interim report on the Muskrat Falls project dated April 8, 2016 (page 13/20) made the following observation concerning the lack of performance based incentives:

5.8 The contract structure was

designed to realize possible savings in construction labour productivity and

also to protect Nalcor from any labour cost overruns that might be experienced

by the contractor. It was intended that this would be achieved by including in

the contract a maximum value for labour that Nalcor would have to pay to the

contractor. However, the payment mechanism is based on person-hours expended

rather than m3 of concrete poured. This mechanism did not capture the potential

for poor contract management of labour and the consequent decoupling of labour

paid for from work completed (measured by m3 of concrete poured). As at

December 2015, the proportion of contract value paid to the contractor is

significantly greater than the proportion of the concrete that has been placed.

EY is describing a contract seriously deficient having decoupled issues of cost and management performance and responsibility. It is surprising that the same observation is not recorded by GT. It would be useful to know if the two accounting firms agree on this and similar problems with the Astaldi contract.

Valard Contract – CT0327 – The HVdc Transmission Line

The award of this work package to Valard included construction of a 1,080km 350kV HVdc transmission line, the Right of Way ("ROW'') clearing from Muskrat Falls to Soldier's Pond together with tower construction and stringing of 350 kV HVdc cable.

The work package, notes GT, was originally four separate packages (CT0327, CT0343, CT0345 and CT0346) but were combined later into one Contract labelled CT0327. The decision to merge the contracts followed on the heels of Nalcor’s decision not to accept a contracting strategy that split the project into a large number of relatively small contracts, as reportedly employed by Hydro Quebec. On this issue, GT reports that Nalcor took the advice of its bankers rather than its Consultant, SNC Lavalin.

In the context of the whole Muskrat Falls Project, the “Construction of HV dc Transmission Line was the second largest work package, accounting for approximately $788 million (20%) of the total cost variance of $3.9 billion as of March 2018”, according to the Forensic Auditor. Adjusted for “transfers from other work packages and scope changes of $139 million the overrun on this work package is $649 million”.

GT attributes this figure to “a combination of factors including contracts awarded in excess of budget, settlement agreement, and change orders due to items such as geotechnical conditions different from planned and the conductor proud strand issue (net of insurance proceeds) and unallocated budget amounts.” (p.41)

At DG3, and Sanction, the Estimate for this work package totalled $735 million including estimated escalation of $62 million. How did the TL end up costing $1.523 billion? The Exhibit (below) offers a breakdown. Puzzling, however, is the line item described as “transfers from other work packages and scope changes”. While GT asked Nalcor for details, it states that they were “unable to confirm the reason for $139 million of those increases.”

If Nalcor knew anything about construction, mega or otherwise, it ought to have been found in transmission line construction. But even here amateur hour is manifest with egregious financial consequences.

GT explains that 40% of the engineering on the TL was completed prior to calculation of the Base Estimate. But Nalcor had not completed any geotechnical examination along the proposed line, not even enough to establish baseline soil conditions which might have helped the estimators. “We had to make assumptions based on mapping…” stated the Deputy MF Project Director. In an interview with BJ Ducey, Senior Vice President, Quanta Services (parent company of Valard Construction) GT records him stating that: "... the actual conditions proved out to be different than what was assumed...” Essentially, Valard used Nalcor’s assumptions to enter into a negotiated agreement through what was termed “open book negotiation” having dispensed with a competitive tender process. Due to unexpectedly poor soil conditions, Valard states that “The assumed family of foundations were not working... "Valard's legal counsel confirmed "That…part of the settlement…reached, is payment for these modified foundations..." (p.47)

In addition, a “number of design changes were made to increase the design reliability and robustness of the HV dc transmission line in the period of 2013 - 2014". Those design changes were a result of "Dark NL". Also coming out of Liberty’s review of reliability issues relating to Muskrat was an acknowledgement “that NL Hydro's operations and maintenance philosophy needed adjustment, and that a near permanent access network would be required…” (P.48) Grant Thornton attributes an additional cost of $212 million for this permanent access road or Right of Way (ROW) including for geotechnical conditions, delays in permitting, terrain and weather conditions.

Notable, too, is that Nalcor succeeded in collecting only $25 million of the $58 million cost having accepted and strung kilometers of a defective or “popped” cable described as “proud stranding”. Strangely, GT does not comment on Nalcor’s Quality Control system that allowed the cable to be accepted in the first place going through several stages of handling and stringing unnoticed.

At bottom, however, as GT states, “Nalcor accepted the risk of geotechnical conditions being worse than what was anticipated in the base estimate.”

As noted, Nalcor did not pursue a “Bid” strategy with this contract. Having reviewed the responses to an RFP, Nalcor concluded that only Valard had the technical and financial qualifications to undertake any of the originally constituted four work packages for the TL. Yet, at the pre-qualification stage, Nalcor states that “We have significant interest in firms to prequalify for CH0007 - at the end 4 bidders were pre-qualified - 3 are international/global firms”. (p.116) It is not clear why this “significant interest” evaporated. GT offers no transparency on the issue.

Engineering, Procurement, Contracting and Management (EPCM)

At the time of Project Sanction, the process of jettisoning SNC-Lavalin as Nalcor’s EPCM contractor was already underway. Nalcor had decided to pursue an “Integrated” management approach to the project. The strategy left SNC only with responsibility for delivering the “E” or engineering design services while the “PCM” portion of “EPCM” was brought in-house, at Nalcor.

This is a very important issue and not just because, from the earliest days, the public was unaware that Nalcor was having problems with its EPCM contractor of a magnitude that, aside from the cost and schedule issues it was facing, represented a sound basis for delay or cancellation of the project. Determined to proceed, Nalcor substituted one “B-Team” for another.

The decision to proceed with an “integrated” management strategy was not announced until March, 2013. Seemingly, SNC-Lavalin had failed to assign competent management to the project at the outset. Rather than look elsewhere for an experienced engineering services contractor, Nalcor essentially permitted the same inexperience that had managed the pre-Sanction activities to also oversee the construction phase, a decision with foreseeable consequences.

The Budget for EPCM services was re-allocated in January, 2014 but EPCM services combined at DG3 amounted to $712 million. By April 2018 the budget for those services amounted to $1.12 billion reflecting, according to GT, cost increases of $406 million.

It is not difficult to discern the knock-on effect of Nalcor’s poor decision-making at the start, including the choice of Astaldi and the decision to proceed with construction of the Transmission Line in the absence of even basic geotechnical testing or data. Having removed SNC Lavalin what did Nalcor do to ramp up quality assurance and control? How much of the $406 million went into quality control? GT does not tell us the answer to this important question. This remains part of the unfinished business which GT must perform before signing off on this forensic audit!

Other Issues:

Other issues covered by GT included the qualifications of the project management team, Nalcor’s contracting strategy as well as the origins and journey of the much-heralded SNC-Lavalin Risk Management Report, brought to the public’s attention by CEO Stan Marshall. That’s the Report, according to some insiders, that was accepted by Ed Martin with “clasped” hand.

This summary will not deal with those issues except in a cursory way, in part for reasons of brevity but also because Grant Thornton’s treatment of them is far more descriptive than analytical. We would like, for example, to have seen more in-depth treatment of Nalcor’s decisions reflecting failures of both processes and people, and their financial impacts. Key among them is the decision to select Astaldi and why their delay in ramp-up, alone, didn’t cause alarms to go off at Nalcor and instigate a replacement.

Other questions that elude are these: was Astaldi solicited by Nalcor or did the Company respond to an RFP? Did Nalcor’s RFP require a “lump-sum” bid? Did any contractor submit a “lump-sum” bid? Were the people who assessed Astaldi’s bid competent to do so? Answers to those questions would constitute just a beginning.

GT also concluded “that the documented policies and procedures governing Nalcor's conduct in retaining and subsequently dealing with contractors were in accordance with best practice.” The Forensic Audit continues: “Generally, with the exception of Nalcor's oversight of Astaldi's work (as described in section 4 of this report), their conduct in retaining and subsequently dealing with contractors did not contribute to project cost increases and project delays.” (P.70)

Frankly, this is a surprising observation. It is difficult to understand how GT can come to such a conclusion when large expenditures are not explained, including the $139 million for the LIL?

Indeed, the major award to Astaldi represents astoundingly poor policies and procedures and is illustrative of the poor judgement which Nalcor’s senior people brought to the project. However, a good many engineers and contractors who worked at Muskrat Falls would not concur with GT’s far too charitable appraisal of Nalcor’s management skills. On this account, the Muskrat Falls Concerned Citizens Coalition might want to begin comparing Nalcor’s safety record at Muskrat against, say, the Hebron construction project.

We had expected more from GT in their appraisal of Nalcor’s actions in managing the project. GT seems content to leave to the Commissioner, through the process of examining Witnesses, to render an assessment of Nalcor’s decisions and to ascribe responsibility for them. Nevertheless, some of GT’s other observations are worth noting even if they contradict the rather soft GT finding just referenced. GT states that:

-

“The core project management team, with the

exception of Ron Power did not have any hydro experience….There were other

individuals on the integrated team that had significant hydro experience,

however these individuals had on average less than 16 years mega-project

experience.”

-

“Nalcor selected a procurement strategy to use

large packages, less interfaces and more risk transfer to contractors. This

decision was contrary to their research…and contrary to SNC's opinion that the

construction packages should be smaller. …..Nalcor has indicated that

financiers preferred larger work packages“.

-

“Nalcor's project risk management policies and

procedures were well defined and documented.” However, GT reports that “From

Sanction in 2012 to 2016, when project risks were materializing, there was no

formal QRA (Quantitative Risk Analysis) process completed.

-

“….while risk registers were maintained, the

overall final forecast cost and schedule did not reflect costs or schedule

changes until they were committed.”

-

“Nalcor…increase(d) the contingency several times

during the project for an approximate amount of $540 million.

-

Nalcor's strategy to mitigate the risk of

"Availability and retention of skilled construction labour" was to develop a

construction schedule based upon "achievable labour productivity." Yet, according to Nalcor's

own risk advisor, there was a 3% chance of Nalcor achieving that schedule.

-

On the issue of the SNC-Lavalin Risk Report, the

Forensic Audit concluded, among other things, V-P Gilbert Bennett and Project

Director, Paul Harrington (and possibly more people from Nalcor) knew the SNC

Risk Report existed and knew that the contents of the report pertained to LCP

project risks. Harrington made a decision not to ask for the report and

recommended to Mr. Bennett that SNC keep it as an internal document in draft

form and not provide it to Nalcor. Mr. Card of SNC remembered discussing the

SNC Risk Report with Ed Martin but the latter has no recollection of it.

This summary and appraisal of the second Forensic Report of Grant Thornton only touches on the larger issues examined even if insufficiently. Nevertheless, we are emboldened by the Report and intend to direct our efforts to ensuring that the issues needing further illumination are brought before the Commission.

Many of the issues raised are unsettling, especially the knowledge that in place of any financial restitution, we can only hope to settle for the truth without any meaningful financial accountability by the perpetrators of this public policy disaster. And that “truth” won’t be arrived at easily. With certainty, a key issue is the disclosure that Nalcor knew, prior to “Financial Close”, that its paltry contingency funding was exhausted, that the project would suffer significant overruns and delay, and still did not bother to inform the public or reassess the implications of proceeding.

We would single out two other issues by way of conclusion.

First, the independence of the Independent Engineer. This is a matter addressed on many occasions by the Uncle Gnarley Blog. One of those included information obtained under ATIPPA to the effect that Nalcor had edited at least one and possibly more of the IE Reports to the Federal Government.

In the current Report, GT also provided proof that Nalcor had been given editorial discretion (p. 16) over at least one Report, resulting in material changes (based upon a comparison of three drafts). Taken together, such interference may have constituted a conflict of interest on the part of Nalcor. Should the IE have refused such changes? What other changes were made in other reports issued by the IE? Did GT review all of the Reports? Did the IE properly inform the Government of Canada on a timely basis as to the existential financial perils facing the project at the start and throughout the construction phase? We believe that these are fundamental questions which ultimately speak to the issue of Federal complicity in the sanctioning process.

The Coalition has written to the Board of Directors of Nalcor concerning the editing of IE reports and we will be filing this correspondence as an Inquiry Exhibit along with the response from the Board. The first phase of the Inquiry is replete with examples where Nalcor and other public officials protected their reputations by interfering with and editing reports from reports which were intended to be independent of Nalcor and immune from their manipulation and falsification!

Finally, there is the matter of SNC-Lavalin. The question raised is this: why did Nalcor remove the Company from virtually every role except engineering design, in spite of its actual world-class record in the management of hydroelectric projects?

Was there any evidence that the SNC Lavalin Risk Analysis was prompted by concern over the Astaldi contract and the award of such a large package to a single contractor? Would this explain the timing of the risk analysis and Nalcor’s strangely defensive reaction in refusing to acknowledge receipt of the SNC Lavalin report?

An even larger concern is that Nalcor had acknowledged the possibility of a $500 million overrun due to identified projects risks. The GT Report, in contrast, (p. 135) confirms that Nalcor’s risk assessment was fundamentally inadequate having failed to fully quantify the risks of the project. GT confirms that “The calculated risk exposure from the SNC Risk Report exceeded Nalcor's calculated exposure by an approximate range of $600 million to $1.7 billion.” (p.136)

Did SNC Lavalin get in the way of Nalcor’s preferred narrative that all was in “alignment” for project sanction? Were the legal troubles hanging over SNC at that time opportunistic, allowing Nalcor to rid itself of a party that might have known too much?

Taken together, is there evidence of malfeasance in the GT Report? Is this an issue better assessed by others or should it be an integral part of the forensic audit?

For our part, we believe that the public deserves answers to the questions which the Forensic Audit raises, all of which are fundamental. That is the very least a democratic society can grant to a citizenry mislead and misinformed both by their government and Nalcor.

The GT report is incomplete and this is no surprise because the project is continuing, with many loose ends that may come apart. The software problem with General Electric is one of the many unresolved issues. The replacement of Astaldi is both unresolved and volatile. We believe it is important that the Commissioner seek from GT a series of progress reports over the coming months, no less frequently than quarterly. We expect that the Nalcor CEO will provide an update when he appears as a witness in June. However the Commissioner will need to have an up to date report from its forensic auditor before submitting his final report at the end of the year. One of the great unknowns which will be disclosed before the Commissioner becomes functus officio is whether first power is achieved on schedule in November of 2019.

Muskrat Falls Concerned Citizens Coalition

Ron Penney

David Vardy

Des Sullivan